IBOR replacement: a major change significantly affecting corporate treasurers

By 2021, LIBOR is expected to be replaced by an Alternative Reference Rate “ARR” as the global interest rate benchmark and this won't be without challenges.

By 2021, LIBOR is expected to be replaced by an Alternative Reference Rate “ARR” as the global interest rate benchmark and this won't be without challenges.

By 2021, interbank rates, such as the London Interbank Offered Rate (LIBOR) are expected to be replaced by an Alternative Reference Rate (ARR) as the global interest rate benchmark. The IBORs (known collectively as ‘Interbank Offered Rates’) are floating rates based on actual or estimated interbank offering rates for short-term loans and have been under challenge for some time. First with the LIBOR Rigging Scandal and more recently with declining liquidity in the unsecured inter-bank lending market, which is the basis for the LIBOR.

IBORs are a cornerstone of the financial industry today, and a transition away from it will impact a vast array of products, businesses, systems, and processes, as well as customers and counterparties. IBORs today underpin the global financial markets and trillions of dollars in financial products are linked to IBORs:

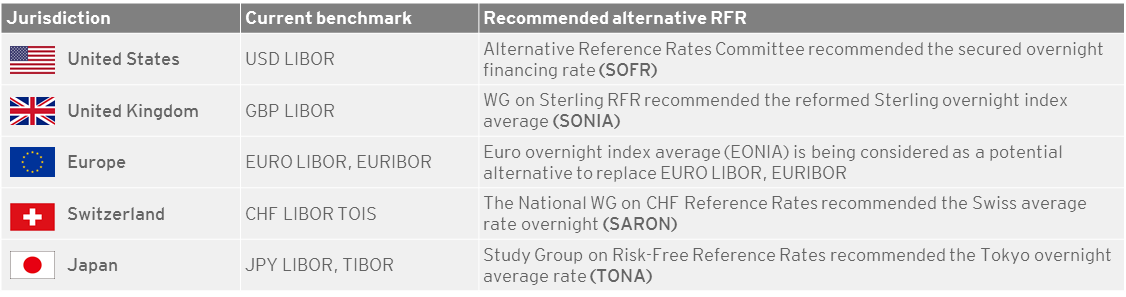

Since 2009, the official sector and market participants have undertaken a series of initiatives to restore the governance and oversight of major interest rate benchmarks and select alternative reference for the IBOR. The new rates must be based on durable, liquid, underlying markets that conform to the International Organization of Securities Commissions (IOSCO) Principles for Financial Benchmarks.

Markets across the globe have taken steps to reform their existing rates in line with the Financial Stability Board (FSB) and the IOSCO Principles. Some jurisdictions have established ARR Working Groups (WGs) to conduct reviews and identify alternative rates:

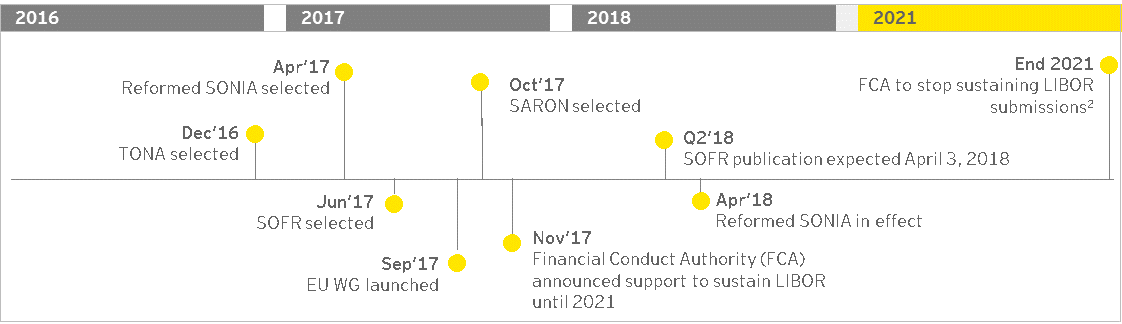

The successful adoption of ARRs is expected to be a multi-annual process. The identification of potential solutions and the design of specific transition plans is at the forefront of the global regulatory community and the private and public sector agenda. The following milestones have been identified to date:

How are corporate treasurers impacted?

LIBOR change is going to affect virtually every corporate treasury dealing with many different dimensions linked to these rates, or any possible nationally divergent interest rates such as the EURIBOR, the CHF LIBOR or the Tokyo Inter-Bank Offered Rate (TIBOR). The effects are significant and will influence broad parts of the organization as these rates are pertinent to the business of a corporate treasury, facing market value exposure to IBORs in its normal day-to-day job.

The fact that new reference rates will not only differentiate from existing IBORs in the way they are calculated, but will defer in their logic and concept, will also lead to material changes in processes and procedures. Changing from IBOR to ARR will not mean that only spreads added to (or subtracted from) the corresponding reference rate needs to be adjusted, the fact that ARRs are overnight rates and currently do not have the same range of tenors as the IBOR rates will impact the entire concept. Additionally, ARRs can be secured and therefore do not include any credit spreads. These are just two examples of how the logic and concept for ARRs will change.

Based on this, one can conclude that key challenges exist across many dimensions for a corporate treasury function:

Cash and liquidity management and bank account management

Corporate finance

Financial risk management

Treasury technology

Tax, valuation, and accounting

In addition, treasury often acts as an internal consultant and sparring partner to the organization when it comes to finance-related matters. Therefore, it should also consider potential impacts on non-core treasury areas such as supply chain and purchasing contracts and processes, working capital management, sales department (e.g. impact on late payment clauses) etc.

Should corporate treasurers be concerned and what immediate actions shall be taken?

No matter how many touch points you have to IBOR, if there is just one, then your immediate priorities for the next few months are to build up a program and start performing impact assessments, covering inter-alia the sort of instruments and processes affected from the rates transition, possible alternative options, but also doing re-thinking of current hedging strategies (incl. documentation). Another important aspect to consider is the creation or adoption of sustainable contracts for the future, having regard to the phrasing of any new types of instruments such as loans, deposits or derivatives being entered into. The year 2021, when IBORs are expected to be replaced, is still far in the future, Nevertheless, taking into account the immense impact that change might have to your business, you are well advised not to wait for too long and to proactively tackle the challenge today.

Sven Göggel is a member of the Swiss Treasury Services competence group and looks after advisory of corporate and insurance clients in all treasury related matter.

Patrick Arcon joined EY 2014 and is part of the Treasury Services team in Switzerland. He has a broad experience in corporate treasury and is a subject matter resource regarding OTC regulations.