We all know the adage about getting what you measure. Well, if the firm could directly measure value creation, then this is what the firm would get! In this article, practising corporate treasurer Ben Walters FCT ACA, explores how the corporate finance ‘holy grail’ may be within everyday reach.

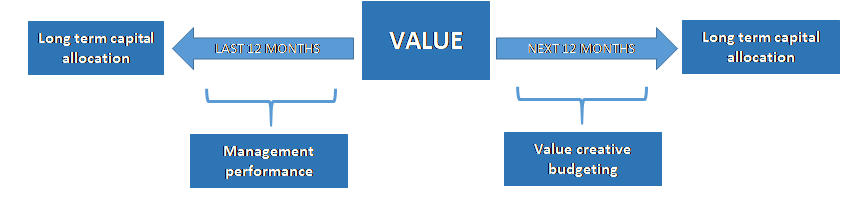

Imagine some of the applications that being able to directly measure value creation could unlock. This could include the ability to:

Set budgets and business plans that create value.

Appraise and reward management performance against value creation.

Shape longer range strategy by allocating capital spend to strategic business units that generate the most value.

Wouldn’t that be great!

Figure 1: strategic uses of value creation measurement

The barriers to getting there however rest in the difficulty of determining the key inputs of value; that of risk and future cash flows. The prize is huge though, with the potential to align the entire firm behind a value creative framework. This I believe could be truly transformative for the role of finance within business and treasurers, as the champions of value, can lead the way in introducing this into the mainstream.

The current state of play

Performance measurement and reward are currently centred around profit and loss reporting. While the sophistication in measurement may have moved on over the course of many years, it remains firmly book based, reflecting historic cost and accruals based accounting and reporting. There are, of course, techniques out there such as Economic Value Add (EVA) that take reported book numbers and adjust these to derive a value created metric for a period.

However, there are disadvantages; EVA for instance can involve miring management and finance teams in a sea of complex adjustments. Taken to the extreme more complex incentive arrangements, such as phantom share options schemes for example, can literally paralyse an organisation as resources are tied up in monitoring and managing the incentive programme.

So, does the firm leave it to the equity markets to decide if value has been created or not? Clearly metrics such as improving profits, revenue and cash flows are all indicators of value creation, but what are the risks being undertaken to achieve these, how much capital has been deployed to deliver these, and how does this performance compare to the market’s assessment of the value the firm should be creating from its strategic position?

To create a process against which value creation can be measured, a little manipulation of the reported data is required. The key principles to get to this stage are to:

accept the principal of working with incremental results,

understand the investment horizon of the business.

Why working with incremental results is the key to an easy life

The simplest way to take out a lot of the “noise” around reported numbers and to focus on the direct effect management decisions have had on the business is to focus on the incremental results. Current levels of profit and cash flow made from past investment decisions is a “sunk” item in corporate finance parlance. For many firms a substantial element of their value comes from the market’s assessment of its future not its past and therefore growth really matters. And of course, if you want to measure and reward performance over a period measure what has changed over the period. Other advantages of thinking in terms of incremental changes are that the effects of inflation haven’t taken hold and the distortions of accruals-based accounting adjustments such as depreciation, amortisation and impairment are minimal.

The effect of working in incremental results is that you only are only focusing on what management is directly responsible for over the period being measured without distortion from inflationary effects and accounting practices. In addition, it is incredibly straightforward; few if any adjustments are required to the reported numbers.

But what precisely should you be measuring?

One of the fundamental assumptions we are taught about corporate finance, that of there being no restraints on capital, is not the case in the real world. Firms tend to generate their own capital or borrow capital. It’s the elephant in the room in terms of marrying corporate finance theory to practise. In this capital constrained world, the hurdle rate for the internal investment decision is always different from the rate of return external investors required if these investors perceive strategic value, i.e. growth potential, in the firm.

This Modified Weighted Average Cost of Capital, or MWACC[1], hurdle rate is the return required when the firm invests capital internally or acquires new businesses. We will explore the concept of MWACC in more detail in later articles, but for now we will use it as the correct hurdle rate in our discussion on measuring value creation.

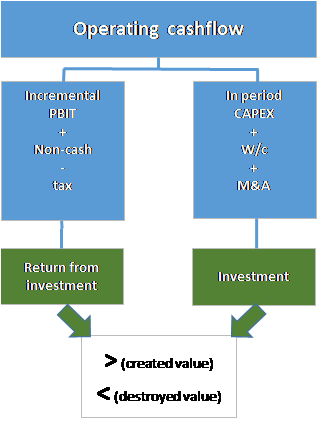

At the strategic business unit level all you need to measure value are the components of operating cash flow, a hurdle rate and an estimate of asset life.

The components then of our valuation are:

Hurdle rate = MWACC

Returns = incremental (year on year change) EBITDA less marginal tax

Capital investment = CAPEX, w/c and net business acquisition and disposal spend

Figure two: measuring value framework

Figure two explains this diagrammatically. The beauty of this technique is that it is incredibly simple. As long as operating cashflow data is available for the Business Unit being assessed, it is simply cutting this data into the “return” and “investment” sides of the coin. Once done if the return exceeds the investment value has been created in the period.

The present value of the return is EBITDA less marginal tax, factored by an annuity based on the average life of the investment made (taken as the average asset life for example). The hurdle rate is MWACC.

In summary the technique is a “top-down” discounted cash flow analysis at the strategic business unit level. Incredibly insightful and informative, but when combined with relevant and directed KPIs a powerful tool to change the firm’s behaviour and deliver value.

Target setting

The beauty of being able to measure value creation from the existing accounting and forecast records is that it is then a very simple process to embed levels at which value is created back into the forecasts and from this set a range of KPIs appropriate to the business and the different operational teams tasked to deliver. For instance, you could set the sales team a revenue target based of the incremental sales needed to generate the incremental EBITDA necessary feed into the value measurement calculation. Return On Capital Employed (ROCE) is another versatile and well understood KPI that lends itself naturally to the value framework. I am sure readers can think of many others, but the point is you have a starting point based on value creation and the KPIs flow from this. KPI’s set from a foundation of value creation have true purpose.

Three further points to make are:

Focus will be on all aspects of capital, including working capital and under-performing assets.

The IRR profile can be scaled to accommodate the timing of expected cash flows.

The of value created or destroyed over several years will show a picture of the success or fail of the strategic deployment of capital over time.

Conclusions

In this article we have developed a framework for embedding value creation into readily available and widely understood KPIs and this has applications for measuring and incentivising management performance, for budget and business plan setting and for longer-term capital allocation (strategy).

Lastly, I have introduced the concept of MWACC as being the correct hurdle rate when the firm is evaluating its own capital allocation. We will explore this further in future articles.

About the author:

Ben Walters, FCT, ACA is a practising corporate treasurer with a keen interest in the practical application of corporate finance in the corporate environment.

He believes finance can support strategic analysis and enhance the overall value of the firm and has developed innovative thinking in this area. He can be contacted through [email protected]