The CFO’s pocket guide to value: part one

One of the biggest contributions a CFO can make to the success of a firm’s strategy is to value it and then break it down into targets

One of the biggest contributions a CFO can make to the success of a firm’s strategy is to value it and then break it down into targets

Strategic choice creates or destroys value, and those of you who have read any of my previous articles will know that I believe strategy and finance should be inextricably linked.

Strategic planning is often seen as a separate discipline to finance, though there is a strong overlap. Our specialism, finance, is great at measuring what has happened, and OK at estimating what we think – or want – to happen. However, it is certainly not great at measuring value. And it barely gets off the blocks when it comes to measuring value and strategy in conjunction with each other. By going back to some basics about the nature of value I hope to build up a picture of how an organisation can translate strategy into measurable financial targets and ensure capital is directed to areas of the business that meet or exceed these targets.

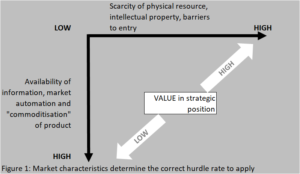

Why market characteristics matter

As figure one shows markets can differ a great deal in the level of information available to participants, the homogeny of the product, and the potential for strategic positioning to create value through differentiation, availability of resources (both physical and intellectual) and barriers to entry.

Toward the bottom left of figure one markets are highly uniform and information is widely available. Barriers of entry are low and assets – both physical and intangible – are easy to replicate. These markets lend themselves to a return built around a statistical measure such as weighted average cost of capital because there is very little scope to beat the market through arbitrage. Stock markets are the obvious and ultimate example of this type of market. The characteristics of financial markets are very different from the much looser and ill-formed markets of the real economy. Unless you are Warren Buffet, countless studies have shown that over time investors should only expect a return from shares equivalent to the general cost of equity.

One of the most useful tasks that stock markets perform from the firm’s perspective is that they estimate the value of the strategy and transmit this information to the share price.

The role of the firm

The firm acts as a conduit between the financial (capital) markets and real assets in the general economy. Business units within the firm generate cash from previous investments and either reinvest this cash back into the real economy or return cash to the firm at the centre. The firm takes this cash, allocates it between business units and then returns surplus cash to the financial markets in the form of dividends and interest. Figures two and three illustrate this.

While figures two and three may seem obvious points my question is this: how many of us appreciate that value means something different to the financial market investor than it does to the firm? It’s true both are concerned with whether the price of the assets acquired goes up or down.

Scarce resources, lack of information, restrictions on capital are often big influences in the real economy. Combine that with the financial market’s role of putting a value on the firm’s strategy and what you have is the situation whereby the firm has to meet an internal return on its investment set by the financial market and usually only using internally generated funds.

So, while the business activities within a firm can create value the big hurdle the firm has to meet is whether these have created enough value to satisfy the demands of the financial market. Wherever the financial market puts a positive value on the firm’s strategy there is the expectation to create capital gains by growing cash flows in the future. Finding that break-even level of return from investments in real assets such that the firm meets the financial market’s expectations is the key to translating the firm’s strategy into measurable business relevant targets.

A final word on value

To the financial market investor value is an exercise in spotting firms where the strategy is undervalued and investing in them before the rest of the market catches up. To the firm, value is about creating, through strategic positioning, situations that allows them to sell goods and services at a higher price than its costs to acquire them. But the point I want you to take away is that just by doing this the firm does not necessarily create value for its shareholders. It only creates value for shareholders if it can beat their estimation of how successfully the firm conducts this business. If it falls short of this the firm’s worth, its share price, falls and value is destroyed. It is not enough for the firm to target the level of return that the financial markets target. That bar has already been set higher by those markets when they estimate the level of growth they expect from the capital the firm retains.

The role of finance and the CFO is becoming much more strategic. At the heart of successfully navigating this path to becoming a strategic partner one of the biggest contributions the CFO can make to the success of the Firm’s strategy is to value it and then break this down into operating targets that drive the business towards fulfilling or exceeding this value. The next article in this pocket guide to value explores how to go about this in practice.

Ben Walters, FCT, ACA is a practising corporate treasurer