What compliance means for electronic invoicing

Although the idea of electronic invoicing is nothing new, implementation of this technology has only been happening relatively recently. This is because electronic invoicing was adopted several years ago in many countries such as those in the Nordics and Latin America. In the Nordics, e-invoicing was introduced to optimise business processes and reduce operating costs, while in Latin America the key driver for change was due to the VAT gap. However, in some other countries, electronic invoicing was introduced more recently or is going to be introduced in the coming months or years. Still, there remains other countries without e-invoicing legislation, so paper invoices are still treated as legal documents.

What’s more, it is very important to keep in mind that digitisation of the invoicing process – replacing of paper documents with electronic equivalents – is just the first step towards invoicing process automation that will result in business process improvements such as higher quality data, more advanced information security, rapid configuration, and improved cash flow.

Many companies planning to implement an e-invoicing process are no longer looking for basic digitisation. They are seeking modern e-invoicing systems that provide a holistic approach to the invoicing cycle and can bring additional value/functionalities that make the invoicing process as automated as possible. This can be achieved, for example, through the use of AI/ML-driven data processing and analytics or by introducing features designed to help facilitate the onboarding process.

This article focuses on legal compliance, specifically what it means for electronic invoices in terms of legal requirements that should be met in order to take the first step towards e-invoicing process automation.

Generally, legal compliance refers to actions and practices that are executed in accordance with the local laws of a country in which a company operates. Going deeper, we can break down legal compliance into two parts: legal and compliance. Legal means local legislation and/or rules, and compliance is about acting in accordance with these requirements.

In the realm of electronic invoicing, legal compliance means acting in accordance with local rules that define how e-invoices can be processed by businesses in a given country.

To be more specific, there are laws that define how e-invoices should be exchanged between parties. This includes rules on the format of electronic invoices, the way they are exchanged (directly or via the tax authority), and archiving (storage period, location of the archive, archive formats).

The following elements should be treated as key points when we consider legal compliance for electronic invoicing:

It should be noted that “tax compliance” is not the same as “legal compliance” when talking about electronic invoicing. Although they are linked, they should not be mixed or combined. This is because legal compliance focuses on how electronic invoices should be processed in a given country while tax compliance is about complying with tax laws and regulations by paying the correct amount in a timely manner.

Legal compliance: the global perspective

As mentioned previously, the e-invoicing landscape is not harmonised across the globe. This is true of the technical aspects of electronic invoicing (i.e. e-invoicing formats) as well as the legal requirements.

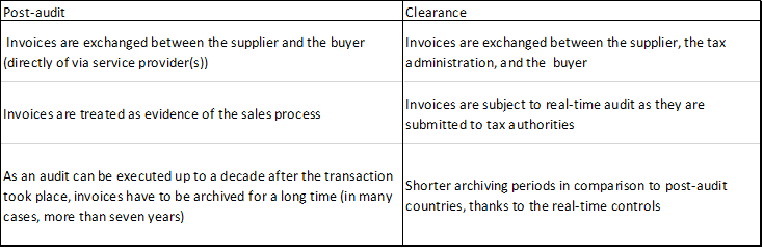

We have already mentioned the significant difference between the Latin American and European approaches. The former uses the clearance approach and the latter generally uses the post-audit approach. The table below shows the main differences between these two models:

What is interesting is that more and more countries are adopting the Latin American/clearance model or something that resembles it. This was the case, for example, in Turkey, which adopted e-invoicing in 2013, and Italy, which implemented mandatory e-invoicing in 2019.

Moving from the post-audit model towards the clearance model is a general trend around the world. Ever more countries are adopting this model as tax authorities want to keep track of all transactions in real-time in order to control tax collection and ensure they can respond appropriately in the event that illegal entries are made in tax reports. The benefits for government entities are, therefore, quite obvious – they can significantly reduce fraud and increase tax collection with ease.

India is an example of a country which is adopting the clearance model

The introduction of obligatory e-invoicing in India has taken place over a few stages. First, it was introduced on a voluntary basis in January 2020. Starting 1 October 2020, it will become fully mandatory for companies with an annual turnover above INR 500 Crore (approx. EUR 65 million).

All companies with headquarters or branches on Indian territory will have to create e-invoices using their own systems and send them electronically to the Indian Registration Portal in JSON format for validation. All invoices get an invoice reference number (IRN) and QR code from which all invoice details can be read. If this process is successful, invoices with digital signatures are then sent to the GST system. The company will then receive proof that the invoice has been registered and the approved invoice will be available for the seller and the buyer on the GST portal.

Other examples of countries implementing the clearance model include:

The regulatory landscape is fragmented. Some countries mandate the use of e-invoices, while others let organisations choose how they want to invoice. The result is regulatory confusion about legal compliance for global businesses. Even among those countries that have embraced e-invoicing, there is often a muddled picture: some use EDI to exchange data, while other countries focus on using e-signatures. E-invoices must be archived and stored for a certain amount of time, but again the length of time varies depending on local regulations. Unless a business is familiar with the regulations of every place in which it operates, it risks running into problems without expert support.

Understanding local regulations is one of the key success factors of e-invoicing projects. One of the biggest issues for businesses is ensuring legal compliance when invoicing projects globally, as each country is different. As a result of this unharmonised and very complex landscape, companies that operate on a global scale quite often incur significant IT costs while setting up to meet local requirements.

Specialised companies such as Comarch can help companies/clients navigate this complex world and overcome the challenges of legal compliance for electronic invoicing. Such experts can help organisations understand local regulations and, more importantly, assist in the deployment of global e-invoicing projects.

It is worth underlining that, by implementing a modern e-invoicing solution, companies can benefit from moving away from paper-based documents; optimising their processes and driving business performance thanks to the modern features of these systems (such as AI/ML-driven data processing, analytics, and features designed to help facilitate the onboarding process). While e-invoicing is not new, what is new is e-invoicing enhanced by modern technology. Companies should not wait for a government mandate to modernise their processes. Instead, they should explore implementing AI/ML-driven invoicing in order to immediately start enjoying all the benefits automation has to offer.