A lesson in agile budgeting

The budget should be a key tool not just in executing the corporate strategy but in enabling it to grow and develop

The budget should be a key tool not just in executing the corporate strategy but in enabling it to grow and develop

What do you really want to achieve from budgeting? Much more than a set of numbers that sit in a column of the monthly management pack I hope. Never has it been more important to being able to set targets, measure performance and maintain financial discipline than in these strange Corona ravaged times. We want to empower those running the business to maximise value. We want to give management the freedom to be entrepreneurial, react in the optimal manner to changes and new opportunities, but maintain financial discipline. The budget is a key tool not just in executing the corporate strategy but in enabling it to grow and develop. The budget is the yardstick by which management performance is measured, and management performance is about creating value.

The annual budget process has traditionally been a very data intensive effort centred around the income statement. Tension between operational and corporate management will usually create some debate and refinement of the “first round” with both sides settling for a compromise position.

Fundamentally this traditional approach to budgeting is one dimensional, focused solely as it is on the income statement (see figure 1). To understand the concept of agile budgeting lets quickly re-cap what firms fundamentally do, at least from a financial perspective. Firms take capital, usually internally generated from retained profit, invest it in real world assets in accordance with its strategy with the aim of creating a stream of future cash flows worth more than the initial investment.

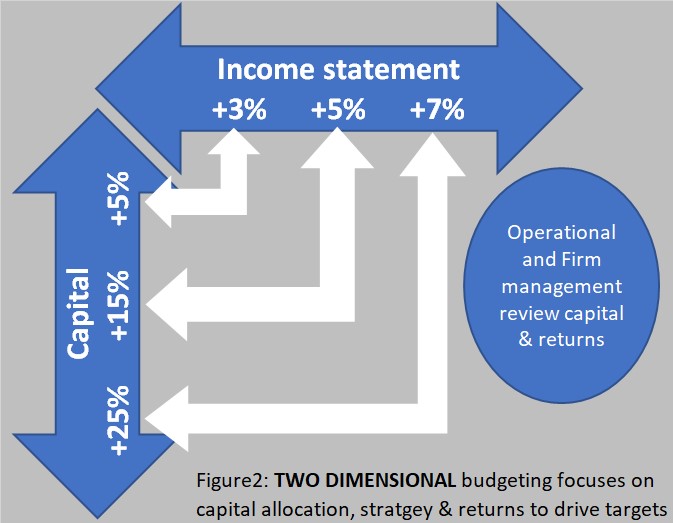

Agile budgeting brings in a second dimension, that of capital, and by doing so creates a framework for setting budget targets based on creating value. The income statement represents the returns side of the equation from the investments the firm makes. The key to agile budgeting is that a balance is struck between the levels of capital required to pursue strategic objectives and the returns necessary to create a positive net present value. Those returns take the form of the income statement agreed as the budget. Two-dimensional budgeting is illustrated in figure 2.

If two-dimensional budgeting is sounding a little bit complicated, then let’s just ground ourselves in some comfortable accounting norms. All you need to implement Agile budgeting is an income and cash flow statement for a business segment that covers the amount of capital invested in that business segment. This data is almost certainly present in any decent general system and should not require too much effort to extract and organise. Agile budgeting is a different perspective on existing data, and it does not require reengineering of the financial nervous system of a business.

The second area where Agile budgeting requires implementation effort is in terms of management education. Change of course can engender resistance, but it is very hard to argue against the principle that returns, and capital are not linked. But with a consistent and transparent framework in place the discussions should centre around the strategy and the efficient execution of that strategy.

An agile budgeting process becomes an exercise in assessing the level of incremental profit a business unit believes it can achieve balanced against the capital they are requesting to help deliver this. Either side of this capital and return equation can be changed: if more profit is required to balance the books then this bar can be raised, while at the same time the amount of capital budgeted can be scaled back to meet the earnings forecast.

Past performance can be measured against budgets of course. But they can also be measured in a much more dynamic manner now. More capital spent than budgeted: well did it create the extra profit that the investment demands? Profit performance can be flexed in consideration of the capital consumed. This allows management to take decisions that create value rather than meet a short term and inflexible budgetary target.

This is certainly not the end of the income statement. But I hope the start of thinking about the income statement as the statement that measures the return on capital and efficiency of the execution of this strategy.

“However beautiful a strategy is, you should occasionally look at the results”, said Winston Churchill.

He was not lucky enough, as far as I know, to have the opportunity to adopt agile budgeting. But you are. Churchill was right: it is very easy to be blinded by the beauty of a strategy and to realise far too late that it is not producing results. This is another area where Agile budgeting can really come into its own. Agile budgeting identifies where a strategy or a strategic business unit is headed. It identifies it in real time, or as near as possible, whether the returns being made stack up against the capital consumed. This is the absolute crux of the matter when assessing whether a strategy is the right one or not. Because agile budgeting looks at returns in a two-dimensional lens forcing the linkage between returns and capital there’s no hiding place if these returns are falling short. You cannot buy your way out of trouble because capital spend comes with a price tag. Figure 3 illustrates a value “heat map” that can be easily pulled together once an Agile budgeting approach is adopted across the firm.

Let’s not stop here though. Resting on our laurels at this stage short changes significantly what agile budgeting can do for your firm. You now have management talking about making the appropriate level of return on capital and being measured accordingly. But this really is just the 10,000 ft perspective. Let’s raise our perspective to 30,000 ft: strategic decisions around capital allocation across business units within the firm can be made by assessing those that exceed the profit to capital equation and those that consistently underperform.

This tells us where we have pockets of value creation and value destruction within the firm. It tells us where the strategy, or the execution of that strategy, is working and where it is not. It allows the firm’s management to allocate capital to the successful parts of the business. It allows capital to be restricted to those parts of the business destroying value and it allows a genuine conversation across the business to share best practice and focus on why and where the strategy is working. Perhaps the explanation is poor execution, poor strategy or a hostile economic environment. The management response can vary depending on the cause, but crucially now the firm can now see clearly where it must concentrate this strategic review. The result ultimately is to improve the overall worth of the firm. Accounting just got clever.