“Capital has the ability to create value from its internal resources be they tangible or intangible, and the purpose given to it my its management. On its own, or in combination with other capital assets, it is able to produce cash flows through a process or operation.” – Ben Walters, deputy group treasurer at Compass Group

Capital does something purposeful. If well managed, it can increase in value independent of the external environment. For example, intellectual property is capital because it represents ideas, patents and connections that can be used to generate cash flows from these properties in the future.

Capital comes with a price tag i.e. an expected rate of return, and the implications of that as finance professionals is at the heart of our roles in the firms we work for. A common term for this price tag is Weighted Average Cost of Capital (WACC). An asset such as cash doesn’t have a cost of capital as its return is based on the risk-free rate and an adjustment for the credit quality of the bank holding it.

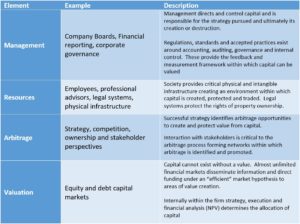

Capital comes with three more critical components which also help define it:

- A requirement to manage it, form a strategy to maximise its purpose and to report its performance.

- An environment where there are resources such as employees, accompanied by a legal and physical infrastructure to allow it to operate and perform its purpose.

- A value, with that function performed, for example, by the equity and debt capital markets.

Lastly, capital exists in an environment in which there are arbitrage opportunities to create value. Arbitrage in an economic sense occurs when there is not a perfect market. These are markets where information is not freely available to all participants and when the flow of funds within these markets might be subject to restrictions caused by regulations, law or a lack of resources. By identifying these arbitrage opportunities, the owners and managers of capital hope to create value.

Capital assets require management to maintain, develop and improve performance. They require a means of measuring performance, and ultimately a valuation based upon this information. Capital requires a framework of critical infrastructure and a system of society that protects its value. Lastly, capital exists in an environment where arbitrage arises from different approaches to management, valuation, resourcing and regulation and gives rise to opportunities to create value.

By defining capital in this manner its leads us to understand our role in treasury in protecting and enhancing its value.

Financial and “real-world” markets

Equity and debt capital markets disseminate information, commoditise the trading of financial instruments and direct the flow of funds in an efficient manner. The financial instruments traded are tokenised pieces of ownership of the capital assets discussed.

These real-world markets are much less efficient than the financial markets in terms of disseminating information and allocating funds for investment.

However, this market inefficiency gives rise to the arbitrage opportunities which a business can identify and exploit. A business can do this by developing a strategy that drives the allocation of funds into capital assets with the purpose of creating value. This process is called strategic planning.

Capital in the real economy

Framing capital in its key elements of management, resources, value and arbitrage allows treasurers to further understand the areas in which to focus on to protect value. The fascination is that every capital asset has unique factors at play under these headings.

The traditional role of the treasurer

Traditionally, treasury has been responsible for the fundamental process of cash management. Cash flows generated within the business are recycled within a business to fund further capital investments or to return to shareholders and lenders. Putting in place the plumbing required to move cash efficiently through the business is a core role performed by treasury.

The quality of forecasting is critical to the cash management process and there is a direct cost to poor forecasting. Underrated and under-appreciated, the value of forecasting is often overlooked. Not just a tool for managing solvency and liquidity, when properly instilled, the forecasting process is the first view a business has as to the success of the strategy being pursued or the quality of management in executing it.

A second traditional role for treasury is that of managing the firm’s capital structure. While in theory there is an optimal capital structure that maximises the value of a business. In reality, capital structure is really more of a credit and shareholder return issue for most businesses.

Lenders and credit rating agencies will look at KPIs such as net debt to EBITDA when determining the availability and cost of lending. And this capital structure decision does not stop at the visible as headroom is a critical safety buffer to ensure a business’ survival. It is often not on the balance sheet, sourced commonly from undrawn committed facilities, but is a critical responsibility for treasury to maintain at adequate levels.

Treasurers manage the flow of funds within a business, promote good forecasting and planning to make this as efficient as possible in the near term, and ensure adequate headroom and back up facilities exist in the longer term.

In the context of our definition of the requirements capital needs to exist, this traditional treasury role can be viewed as an element of resourcing of capital by ensuring funds exist to meet the business’ immediate and longer term demands for capital. The distribution of excess funds to shareholders and lenders plays a part in the valuation of capital, as efficiency here ensures that as little as possible of the internally generated value from capital is lost when cash is returned to the business’ owners.

The non-traditional role of treasury in managing capital

But a treasurer’s role should not stop at these traditional responsibilities. The treasurer can contribute in unique areas to that overriding purpose of the business to protect and enhance the value of its capital.

Getting the cost of internal capital decision correct has both technical and behavioural implications. The next article in this series will explore the importance of this area in some depth and introduce a new technique to arrive at this cost based on meeting and exceeding the external expectations of a company’s growth. My modified WACC concept defines the internal rate of return a business must achieve on its internal capital allocation in order to justify the external valuation placed on the company overall.

While financial reporting focuses on profit and earnings, successful performance is ultimately about the creation of value and not profit. This disparity can be bridged because value and profit are simply two sides of the same coin. Value measurement is a holy grail in financial reporting terms, as it involves the extra dimensions of capital invested and risk. These are not elements of the traditional reporting toolkit, but they can be easily and seamlessly adopted within one. The business can set performance targets rooted in value creation from the capital it consumes. Treasurers are ideally placed to apply the lateral thinking required to bridge the gap between internal performance targets and those placed upon the business by the external markets.

Lastly, a business must allocate capital towards the best arbitrage opportunities and restrict or withdraw capital from those activities that destroy value. The treasurer is uniquely placed to orchestrate the process of capital allocation in an analytical manner to add tangible support to the strategy process.