SOFR gaining momentum as drop dead date for Libor nears

Transition from US dollar Libor to its preferred alternative, SOFR, is going surprisingly well, though treasurers are having to grapple with some operational issues

Transition from US dollar Libor to its preferred alternative, SOFR, is going surprisingly well, though treasurers are having to grapple with some operational issues

With just over a year to go before the death knell is finally sounded for Libor, evidence is mounting that banks and borrowers are decisively moving away from the legacy reference rate, with transition from high profile US dollar Libor to its preferred replacement, the Secured Overnight Funding Rate (SOFR), especially encouraging.

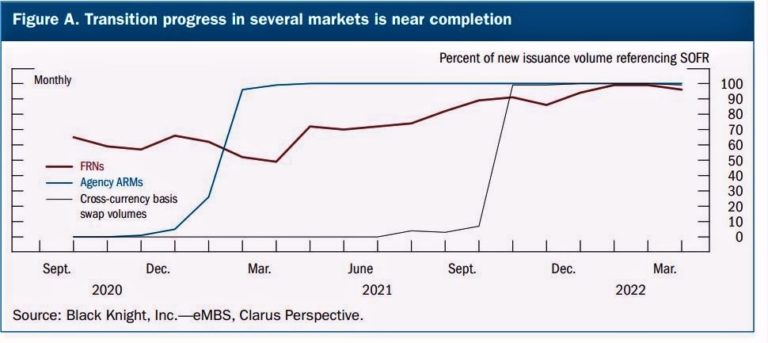

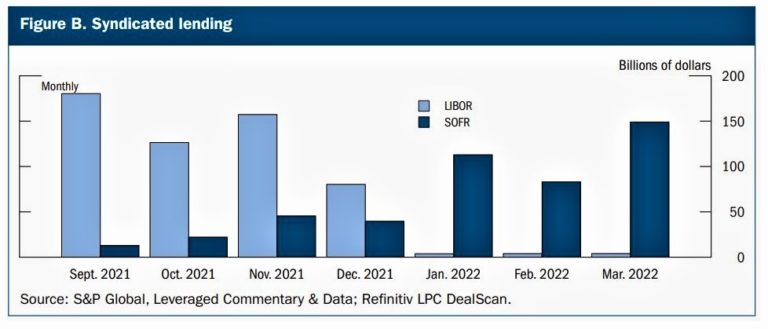

The good progress with SOFR was hailed earlier this month by the US Fed in its bi annual Financial Stability Report. According to the US central bank, there has been a “clear shift” away from US dollar Libor since the start of the year across business loans, securitisations, floating-rate note markets and interest-rate swaps trading. Syndicated loans were slow to get off the mark in transitioning but by early 2022 had shifted almost entirely to SOFR-referenced products. Assessments of non-syndicated loans, meanwhile, indicates most banks have reduced Libor lending sharply since the start of the year, with most loans now referencing SOFR.

With Libor tied to more than $300trn of contracts globally and nearly $200trn of US dollar contracts, the transition to alternatives amounts to one of biggest ever challenges for the financial services industry. The outsized US dollar exposure to Libor means progress with SOFR is keenly watched by the financial services sector, not least by US-based financial risk manager Chatham Financial, which offers corporates expertise in the debt and derivatives markets, including execution services.

Kevin Jones, director of treasury advisory, says one challenge being faced by both lenders and borrowers alike is the emergence of various versions of SOFR, spanning debt, derivatives, and hedge accounting treatment, which has introduced “considerable ambiguity” to the path forward. At the same time, with legacy debt and derivatives based on Libor able to persist until June 2023, borrowers are left grappling with the tension of taking action now versus waiting to cutover to SOFR.

Indeed, says Jones, progress with the transitioning to SOFR is best viewed in terms of the contrasting experience of lenders on the one hand, and borrowers on the other.

“Banks as primary lenders have pretty much fully transitioned. There are no new loans on Libor and trades between banks are generally on SOFR. It is the Libor borrowers – our clients – that are still mainly in this process of transitioning over,” he says.

Jones says many companies still have legacy Libor debt and, absent some trigger event that would force them away from Libor such as a refinancing or upsizing of their debt, are in no rush to change it over to SOFR.

“What we are seeing now, however, is companies start to borrow and use SOFR to hedge their interest rate risk. By mid-2023 when LIBOR officially goes away, those companies which are exposed to US dollar Libor and have not had a trigger event in the interim will automatically cut over to SOFR or one of its variants and that will complete the transition.”

Amol Dhargalkar, managing partner at Chatham, says there are several reasons why a company would want to wait to refinance and thereby trigger the move away from US dollar Libor.

“If the company refinanced just a year ago they may, understandably, be reluctant to do it again so soon, especially as there will be costs to consider,” he says. “It’s one of those situations where we [at Chatham] aren’t necessarily advising them to refinance now or refinance later. It has much more to do with the company’s capital structure and strategy, it’s not a decision built around Libor. Libor is an element of that decision making process but it’s by far nowhere near the driving factor.”

As for derivatives, if they are Libor-based, Chatham is generally advising clients to utilise Libor-based derivatives to hedge the debt rather than creating some type of economic mismatch between a SOFR-based derivative and a Libor-based derivative. However, says Dhargalkar, there are situations where companies are not necessarily able to opt for Libor-based debt.

“An example here is swapping a bond back to floating rate,” he says. “That is a not a scenario where companies can opt for Libor-based derivatives any longer as that is now usually SOFR-based.”

Looking ahead to the scenario for companies come June 30, 2023, Jones says most will have language in their loan agreements to affect an automatic cutover of their debt to SOFR. It will be more nuanced for derivatives as there will be a few different mechanisms to force through their transition.

“With derivatives, I think we’ll see a lot of attrition of Libor trades by the time Libor actually comes to an end but there will be significant number left that will have to automatically cutover to SOFR in June 2023,” says Jones.

“Also, as we approach that cut-off date, you might see companies more proactively moving away from LIBOR derivatives. Right now, there’s not a strong case for that, a trigger event like a refinancing. But you might start to see more companies realise that it makes sense to do that as June 2023 approaches.”

One area where there has been substantial cutover to SOFR already is investment grade (IG) corporates looking to swap fixed rate to floating rate debt, according to Dhargalkar.

“Previously that action didn’t really require a long conversation, they would just swap to LIBOR, or some variant of LIBOR. Late last year though, banks started to say they can’t even do that anymore, that it had to be SOFR derivatives not Libor derivatives. So that’s an example of where the cutover has essentially already happened. Theoretically you could price Libor derivatives in those instances but the price won’t be made from a regulatory standpoint.”

Jones says that with most situations the aim at Chatham is to match the client company’s underlying debt with the right type of derivative. That typically involves a lot of advisory, not least as SOFR comes in several different flavours. Predominant among there are CME Term SOFR, which like Libor is a forward-setting term rate. Beyond that are other iterations including Daily Simple SOFR in arrears, which is calculated using simple interest over the current interest period; and SOFR compounded in arrears, which is calculated by compounding interest over a previous set amount of days.

One of the biggest concerns for Chatham client treasurers and CFOs is the operational impact of benchmark SOFR being a backward-looking rate based on the cost of borrowing cash overnight collateralised by the US Treasury securities in the repurchase agreement market. As it is a backward-looking rate, it can only be published in retrospect. This regime is quite a change from Libor, which is forward-looking, with the benchmark rate known at the beginning of each interest period. Adjusting to a backward-looking regime, owing to the Libor transition, poses the risk of uncertainty and computational problems.

“If, for example, you are swapping a fixed rate bond back to floating, the benchmark for that is a compounded daily rate,” explains Jones. “The disadvantage is you don’t know what your rate is until the end of a period. And then there’s a payment due two days later. That can be a very challenging, operational consideration for companies, especially those with limited resources. And it’s a general issue, not just limited to swapping to floating.”

Source: US Federal Reserve Financial Stability Report, May 2022

Source: US Federal Reserve Financial Stability Report, May 2022