Just over a year ago, I published a piece titled ‘Interest rate risk: fixed or floating‘ on the fixed versus float interest rate decision that forms the heart of many corporate treasury interest rate risk management policies. A review of historic data concluded that:

- The majority of the time, c.75%, it pays to be a floating rate borrower over fixing a rate, for any given three-year period in major currencies such as USD, EUR or GBP

- However, we identified times, specifically at the start of central bank rate hiking cycles, when a fixed approach over a three-year period paid off instead.

- These fixed pay-off periods were reinforced when negative real interest rates also prevailed.

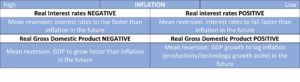

The rationale for why this is the case comes from considering what real interest rate and real Gross Domestic Product (GDP) tell us about supply and demand for cash coupled with the concept of mean reversion over time. The idea of mean reversion is that GDP should match and slightly exceed inflation over time (the excess arising from productivity and technological gains). Interest, the price of cash, is intrinsically close to zero in real risk-free terms, so in nominal terms should match inflation. When we see the price of cash or GDP move away from trend, which we do constantly, the expected future path should eventually follow this mean reversion rule. Of course, the timing of this move is unpredictable, and the factors that drive the momentum of interest and GDP into positive or negative territory can exist for many years. I have summarised this in the table below:

What do these measures tell us today?

I have reproduced figure two from my original article, updated now with data from the past year. This is a USD plot; however, other mainstream currencies show exactly the same trends.

The very basic “fix or float” rule I developed can be clearly seen in this chart: fixing only pays off (in interest cost terms of course, there are other benefits to the borrower) at the start of a rate hiking cycle. In addition, this effect is slightly stronger when the start of the rate hiking cycle also coincides with negative real interest rates.

Historically we had a period from 2003-2005 and from 2015-2017 when both these factors coincided and fixing an interest rate for three years in these periods turned out to be cheaper than accepting floating rates over the same. If we look at the far right of the plot now it is very obvious that the rate hiking has started, and that the negative real interest rate prevailing is almost off the scale. According to our rule, this is an extremely strong “fix” signal.

Have your say… Take five mins to complete The Global Treasurer’s Audience Survey 2022

So what else is going on?

As I write, poor economic news from the US that inflation has failed to “peak” in May has prompted revisions upward of interest rate hikes and the chances of recession in the developed world. Inflation since the turn of the year has taken off – surprising the markets and central banks, and confidence about when it might peak is being tested.

Below we look at several forward-looking factors across USD, EUR and GBP. However, to point out across all three currencies the shape of the yield curve is currently “humped” which is a classic sign of volatility and recession.

USD

From a baseline level of deeply negative interest rates and GDP, both are set to move positively with interest rates becoming positive in real terms in around two years from today. GDP is forecast to recover at a slower rate. This could suggest that interest rates may not rise as much as predicted from year two out, as real GDP will still be in slightly negative territory at this point while inflation is predicted to drop back to around the long-term target rate of two percent. The US Federal Reserve may accommodate lower interest rates at this point to boost the economy.

EUR

Deeply negative real interest rates are set to undershoot negative real GDP for the next year and then return to positive territory in around year two. Inflation is forecast to return to two percent from around year three. This pattern could suggest that rates might rise quicker than forecast in the short term of up to a year and thereafter may not rise as high as forecast in years two and three as real GDP remains slightly negative in this period and inflation comes back under control. Again, the European Central Bank may be looking to support the economy more than rates predict if inflation is back under control.

GBP

The major difference between GBP and the EUR and USD data is that inflation is forecast to remain elevated at around four percent in year two onwards. At the same time, real GDP remains significantly further into negative territory across the period. This negative real growth and high (in relative terms) inflation environment makes any path for interest rates very hard to forecast. There is the distinct possibility that the Bank of England may need to retain an accommodative stance in order to avoid a deep recession though the weak pound will contribute rampart imported inflation.

The treasurers perspective

Although the analysis above pulls together some of the key factors feeding into the possible path of interest rates over the next couple of years, and whether the market has got this right, it is important to set this discussion very firmly within the context of the business.

Some businesses can react swiftly to high inflation, high-interest rate environments, increasing their revenue and maintaining their margins – others cannot. Of course, the interest cost is important, but treasury should really be judged on the appropriateness of the policy to the business. If the policy does allow room for judgement then the quality and rigour of that judgement can and should be assessed but beating the market should never be part of the corporate treasurer’s remit.

DISCLAIMER: Nothing within this article should be taken as advice or any form of recommendation. The views and conclusions expressed are purely those of the author acting in an individual capacity.