Rising rates make intraday liquidity even more interesting

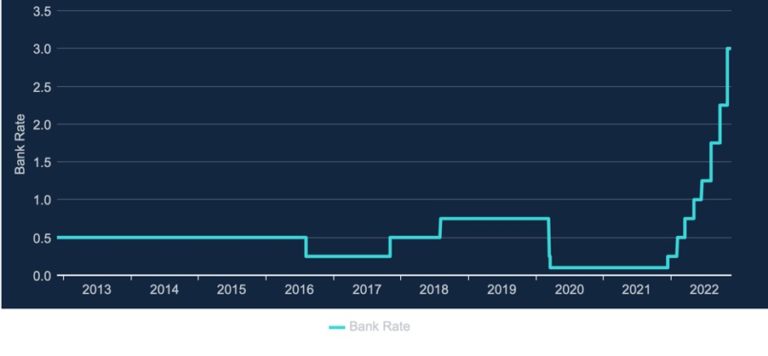

One of the more ‘interesting’ aspects of 2022 for a treasurer has been dealing with huge interest rate increases with the expectation they won’t be coming down any time soon. Figure 1 shows how GBP base rates have changed over the last 10 years, other major currencies show similarly painful patterns.

Figure 1 – source: Bank of England database

Figure 1 – source: Bank of England databaseI am going to concentrate on how rising rates influence intraday liquidity (IDL). I’ll start with a reminder on what is IDL, why it’s important, explain how rising rates cause problems, and suggest how you might respond. IDL is generally more important for bank treasuries than corporates, but ultimately higher IDL costs for banks will find their way back to those clients using this IDL!

Imagine you are a vanilla financial institution, like a bank clearing in local currency with nostros at agent banks for your business in other currencies. You might have deposit accounts at venues to manage securities, but for now let’s just think about your cash accounts.

These accounts allow you to pay and receive money to support your bank’s business activities. Since you might have to pay money out before receiving money in, you need access to liquidity during the day. You access such IDL either via an account overdraft or by providing enough prefunding to make payments before money starts to arrive. Figure 2 shows how pay early/receive late behaviour requires significant IDL to complete the day.

Because it’s existential, costly and of interest to regulators.

Why existential? Because liquidity is the lifeblood of the firm. Firms go bust if they don’t have liquidity when they need it most, i.e., when they need to make payments intraday. Lehman Brothers died as it didn’t have enough liquid assets to meet its outflows and couldn’t source enough intraday credit to fill the gap.

It’s costly for multiple reasons associated with using too much liquidity: certain account providers charge daylight overdraft fees; there are costs associated with securing a credit line; there are overnight interest costs if inaccurate funding assumptions mean you finish short at the end of day.

Depending on your location, regulators focus on ensuring you understand your intraday needs, how requirements might increase under stress and hence how much (expensive!) liquidity buffer should be dedicated to cover intraday needs.

When rates are low so are liquidity costs. Your bank might have spare liquidity available for IDL, as you have limited options to use excess cash. Similarly it’s easy to access cheap credit from account providers as they too have excess liquidity with little appetite in the market to buy it. But interest rates are now rising while central banks introduce quantitative tightening to remove liquidity from the economy.

This is when ‘lazy liquidity’ becomes problematic. Lazy liquidity is where, because liquidity is almost ‘free’, you simply park cash at the central bank and also deposit large cash balances into nostros at the start of day just-in-case it might be needed. But with rising rates lazy liquidity starts to cost you. Now you can make money on any spare liquidity rather than leaving liquidity trapped earning minimal returns. As rates increase, opportunity costs increase too as the front office can do much more with available liquidity rather than treasury leaving it trapped in low-yield locations.

For similar reasons, your account providers will be much more reluctant to provide free intraday liquidity and will take actions to address this. This could be one or more of: explicit charging for ILD usage, charging for providing a credit line, asking for your IDL usage to be collateralised. All of these actions increase your costs of funding your account activity.

Where you have an intraday liquidity buffer, rising rates means the costs of providing such a buffer will be more expensive. Such buffers can be eye-wateringly expensive; for each $1bn of liquidity buffer an extra 100 bps on buffer charges will add $10m of annual cost!

For all the reasons just discussed here you should expect counterparties to become expert at managing their IDL usage and payment profiles. If you are exposed to the other side of their smart behaviour you might end up providing counterparties with free intraday liquidity. It’s an expensive mistake to be the unknowing patsy allowing others to freeload on your IDL.

IDL only really became a mainstream topic after the Global Financial Crisis. Since then interest rates have been historically low, but no longer. For many people working in treasury today this is the first time they have been thinking about IDL while also worrying about rising rates.

Given higher rates are now here and are likely to stay high, treasury must optimise actual IDL usage. This starts with understanding IDL profiles and identifying drivers of ILD usage. You can then, as much as possible, reduce that intraday usage. All this starts by gaining what is known as Intraday Control. Intraday control means you can monitor all your accounts of interest in real time, compare what is actually happening intraday to what you think should have been happening at this moment (the forecast) and if there is a difference then manage the intraday risks as they crystallise. Intraday control gives you intraday insight and you can use this insight to make the best decisions possible in terms of allocating liquidity, funding accounts and supporting settlements.

Once you have intraday control then you can start to influence high IDL usage. There are a range of options here: transferring costs of IDL to those business units generating the IDL usage hence driving behaviour change, finding ways of profiling payments to minimise IDL short positions, encouraging customers to optimise their IDL behaviour etc. Intraday control relies on having the right data, systems and processes.

Please take a look at Realiti® from Planixs for inspiration!