The life insurance sector has undergone a significant transformation over the past decade, with private equity (PE) firms emerging as major players in an industry traditionally dominated by long-established insurers. A recent study by the Bank for International Settlements (BIS) reveals that PE investment in life insurance has grown nearly sevenfold since 2010, outpacing PE investment growth in other financial sectors.

This surge in PE activity has been particularly pronounced in the United States, where PE-linked insurers have become increasingly prominent. The BIS report notes that by the end of 2023, PE-linked life insurers in the U.S. had ceded risk to affiliated insurers equivalent to almost half of their total assets, amounting to nearly $400 billion. This stands in stark contrast to other U.S. life insurers, who ceded less than 10% of their total assets.

Several factors have driven PE firms’ growing interest in the life insurance sector. The prolonged low interest rate environment following the 2008 financial crisis created challenges for traditional insurers, particularly those with legacy policies offering high guaranteed rates of return. This situation provided opportunities for PE firms to acquire undervalued insurance assets and implement new strategies to boost returns.

PE firms have pursued various approaches to enter the insurance market. These include acquiring existing life insurers, establishing new reinsurers to take over blocks of policies, and providing asset management services to insurers. The BIS study highlights that PE-linked insurers were “twice as likely to invest in assets originated by PE firms compared to other insurers,” indicating a significant shift in investment strategies.

One of the key ways PE firms have sought to generate higher returns is by directing insurers’ investments into less liquid and potentially riskier assets, particularly in private markets. The report states that “PE-linked insurers’ investments are often less liquid and more difficult to value, with notably larger shares allocated to structured credit.” While these investments may be well-suited to match long-term policyholder commitments, they also introduce new risks, including potential valuation uncertainties and increased vulnerability to unexpected outflows.

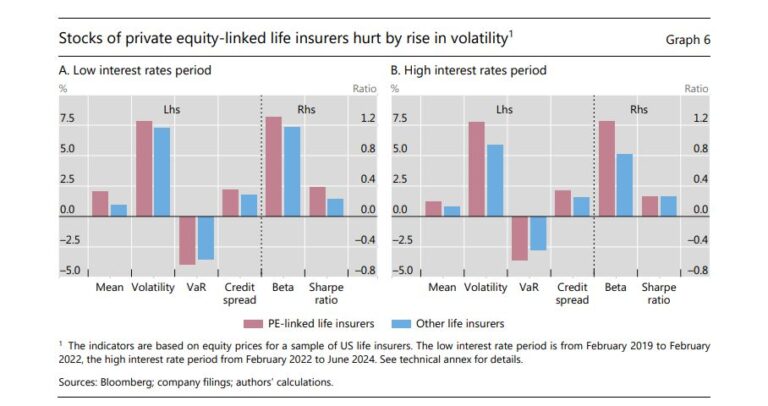

The performance of PE-linked insurers has varied depending on the interest rate environment. During the low interest rate period, PE-linked insurers significantly outperformed their peers, with mean returns more than twice as large and Sharpe ratios around 50% higher. However, as interest rates have risen, the picture has become more complex. The BIS study reports that “in contrast to their peers, the volatility and betas of PE-linked insurers stayed elevated, and their risk-adjusted returns fell while still exhibiting larger tail risks.”

The growing influence of PE firms in the life insurance sector has raised several concerns among regulators and financial stability experts. One key issue is the increasing complexity of reinsurance chains, often involving offshore entities. The BIS notes that “about two thirds of the risks ceded by PE-linked life insurers were assumed by affiliate reinsurers with links to PE located in offshore centres.” This trend has made it more challenging for supervisors to assess how risks could propagate through the financial system.

Another concern is the potential for conflicts of interest, particularly where asset managers, including PE firms, have incentives to allocate insurers’ funds to assets they originate. The BIS warns that “the risks are magnified given the potential for strategic mispricing of illiquid and hard-to-value assets.”

The concentration of risks in a relatively small number of reinsurers and jurisdictions also poses potential stability risks. Unlike traditional life reinsurance, which benefits from diversification of mortality and longevity risks, the BIS points out that “returns on invested assets could prove highly correlated in the event of widespread market downturns.”

These developments present significant challenges for regulators and supervisors. The BIS emphasizes that “supervisory monitoring has become more complex owing to cross-border risk-sharing arrangements among or within large (re)insurance companies and their connections with PE firms.” The report calls for enhanced international supervisory cooperation and more robust regulatory standards to address these challenges.

Looking ahead, the resilience of PE-linked insurers and their investment strategies remains to be fully tested in more challenging market conditions. While PE firms have brought innovation and fresh capital to the life insurance sector, their growing influence also introduces new dynamics that regulators and market participants will need to monitor closely.

The transformation of the life insurance landscape driven by PE firms represents a significant shift in the industry’s structure and risk profile. As the BIS study concludes, these developments “underscore the importance of rigorous group-wide supervision, systemic risk analysis and international cooperation” to ensure the continued stability and integrity of the life insurance sector.