Why Venture Debt is No Longer Just a Bridge, But a Strategic Growth Tool

The era of cheap equity is over. Venture debt has shifted from being a financing bridge to a strategic, non-dilutive lever for growth. Here’s why late-stage companies are now embracing debt discipline to extend runway, preserve equity, and control their future valuations.

The playbook for funding high-growth companies has fundamentally changed. After a decade-long spree of “growth at all costs” fueled by cheap equity, the current economic climate—defined by higher interest rates, restrained VC spending, and a stalled IPO market—has ushered in an era of capital efficiency and discipline.

In this new environment, venture debt has moved from the periphery to the center of the strategic finance conversation. No longer viewed simply as a last-resort bridge loan, it is now an indispensable instrument for mature startups seeking to fuel expansion without surrendering valuable equity.

For CFOs, Treasurers and founders navigating this transition, understanding the new realities of the venture debt market is paramount.

The Paradigm Shift: From “Rescue” to “Discipline”

The most significant change is one of perception. Recent industry reports show that the decades-old stigma of venture debt as “rescue financing” is rapidly fading. Today, for companies with product-market fit and reliable, recurring revenue, securing a venture debt facility is increasingly seen as a sign of financial sophistication and discipline.

This shift is driven by a simple, powerful calculus:

1. Preservation of Equity is Paramount

With IPO timelines at their longest in a decade and valuations reset from their 2021 peaks, founders are extremely focused on avoiding dilution. Venture debt allows a company to significantly extend its cash runway—often by 12 to 18 months—and hit critical operational milestones before facing the equity market again. This is the ultimate goal: raising a subsequent equity round at a higher valuation, thereby minimizing dilution for existing shareholders.

2. A Focus on Late-Stage, Strategic Growth

The market is concentrating its resources. Data suggests the bulk of new venture debt financings are occurring at the late-stage or venture-growth phase. Lenders are increasingly selective, favoring companies that have proven their business model and can demonstrate a clear path to profitability. This is not capital for early-stage experimentation; it is fuel for scaled execution.

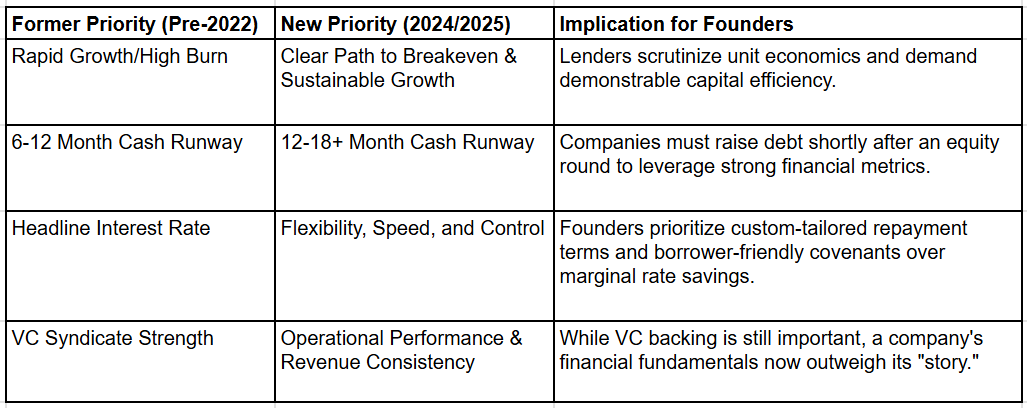

The New Lender Playbook: What Lenders Prioritize Now

Lenders, having navigated a period of volatility, are more cautious and pragmatic than ever before. To successfully secure a facility, companies must align their financial strategy with the evolving priorities of capital providers:

The takeaway is clear: companies with predictable revenue streams, particularly in SaaS, Fintech, and Healthcare, are the most attractive candidates. Their recurring sales models provide the necessary visibility for lenders to underwrite risk effectively.

Venture Debt as a Treasury Strategy

For the forward-thinking CFO, venture debt is a critical component of a modern treasury function. It’s a tool to be used proactively for:

Acquisition Financing: Funding tuck-in M&A without tapping the core equity budget.

Working Capital Buffer: Creating an insurance policy to weather unforeseen market shifts or extend runway if a major equity round is delayed.

In a market where how you raise money is often more important than how much, venture debt has positioned itself as the definitive non-dilutive solution for growth-stage companies.

By embracing capital discipline and demonstrating a clear, efficient path to scale, founders can successfully wield this strategic lever to control their destiny and maximize shareholder value.