How banks can accelerate efficiency for SMEs with Virtual Account Management

Virtual Accounts key to banks effectively supporting the needs of SMEs, according to Justin Silsbury, lead product manager at Infosys Finacle

Virtual Accounts key to banks effectively supporting the needs of SMEs, according to Justin Silsbury, lead product manager at Infosys Finacle

SMEs account for up to 99 percent of all the companies in Europe. Surprisingly though, banks have underserved these customers and focused more on retail and the larger corporate clients. However, is it correct to assume that most SMEs only require a retail like experience anyway? This maybe be correct for the smallest SMEs who are happy to be left alone but many businesses that fall into this category can have far more complex needs. The internet has had a major influence in terms of both speed and expansion, with SMEs able to leverage the internet to establish a global presence with relative ease. Such customers require a bank that will enable them to run their business successfully by providing a range of different products to help optimise their working capital.

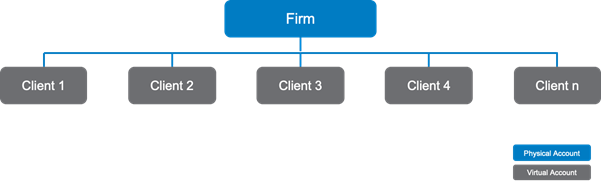

One such product that has advanced in line with technical innovation is Virtual Accounts, which enable companies to rationalise their bank accounts significantly. It allows reduced reliance on intraday credit by managing transaction flows and liquidity positions more efficiently, by moving from a multibank account, decentralised structure to a centralised structure with increased visibility and control. Modern virtual account management (VAM) offerings from progressive banks ensure high self-service to address several different customer needs, allowing reconfiguring of sub-ledgers and designing a virtual account hierarchy that directly reflects their business needs.

Following are a few use cases on how the different SME customer needs can be addressed with VAM.

Use Case 1: Client Money Management for SME Firms

Client Money is money that an SME holds or receives for or from a client and can be of any currency. Regulated professionals such as legal, accountancy and insurance firms require a safe but simple way of segregating their clients’ money. The SME can operate a single physical account in a particular currency and link virtual accounts for each of their customers. If agreed between the SME and customer, interest terms can even be set on the virtual accounts. This use case can also be extended to escrow where the SME is holding money on behalf of two other parties that are in the process of completing the transaction.

Use Case 2: Landlords

A landlord is the owner of a house, apartment, land, or business premises which is rented to an individual or business. Landlords can have single properties that they rent out or can run into the thousands. By creating virtual accounts for each of their tenants landlords can provide unique payment instructions which will allow the tenant to pay to the physical account and then replicated to the virtual account.

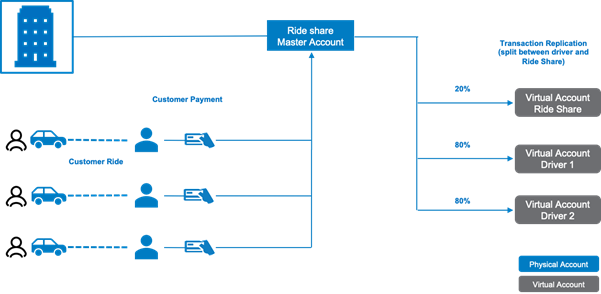

Use Case 3: Taxi companies

Whether a taxi company, executive car hire or any business where a company brings in independent contractors, a simple virtual account structure can be created. Here, the contractors are paid through a card reader device which is linked to the companies physical account and replicated to the virtual account for the individual contractor. The payment can even be split between the business and the contractor at a percentage agreed between the two parties.

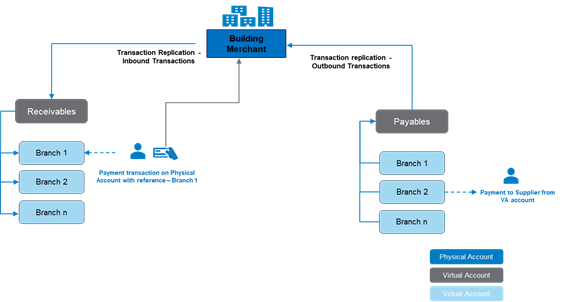

Use Case 4: Building merchant

Larger SMEs may have a business with a number of branches located across a country, region or even globally. However, as these businesses grow they need solutions from the bank that can grow with them. Virtual accounts can be created in hierarchy structures that mimic the company’s structure. As an example, a business can set up virtual accounts for payables and receivables for each of their branches. Customers will make payments to the company’s virtual accounts while suppliers can be paid from the payables virtual account linked to the branch.

Overall, a VAM solution can enable SMEs to manage their operations efficiently, streamline payments and receivables, while greatly reducing the costs. Banks will need to ensure clients have access to a whole lot of traditional global cash and liquidity management solutions, along with the much-needed flexibility and self-serve capabilities. Banks stand to benefit too by enabling the shift in controls to the end SME user, helping them better manage their global, multi-bank cash and liquidity requirements. The Finacle VAM solution is an industry leading solution designed precisely to help banks delivery such services and help simplify SME accounting and treasury management practices. With a broad range of account virtualisation capabilities and digital self-serve model, the solution enables a business to grow its footprint while maintaining enhanced levels of visibility and controls.

In closing, one point requires enunciation though – virtual accounts are an integral part of a larger suite of solutions related to liquidity, payments, collections and channels to help improve working capital and reduce the cash conversion cycle.